HOW TO COMPARE MORTGAGE OFFERS

Shopping around for the best mortgage offer can be overwhelming. We would like to explain a few things that will help you simplify this process and help eliminate all of the stress and confusion that you may experience when comparing rates and fees with various lenders. If you want to skip all of the technical stuff, you can scroll to the bottom and get the simplified version of how it all works.

Where Do You Start? How To Shop For a Mortgage

There will be lots of loan disclosures when applying for a mortgage. For now you can disregard all of them and focus on only one document called the “LOAN ESTIMATE” sometimes referred to as the “LE‘. This document is similar to what used to be called the Good Faith Estimate. The loan estimate will tell you everything you need to know about the interest rate and fees that the lender is charging. It is the only document that you’ll need when shopping for the best mortgage offer. Please note, there are many other important loan disclosures that consumers need to be aware of but for the purposes of comparing loan offers, there is no document more important than the Loan Estimate.

It is important to note that a lender will often not provide a Loan Estimate until the consumer has provided them with additional information such as a property address, credit scores, income, etc. In fact, by law, a loan estimate is only required to be provided once the bank has 6 pieces of information which include the borrower’s name, social security number, property address, estimated loan amount, consumer’s income, and estimated property value. Once the bank has these 6 pieces of information, they have 3 business days to disclose a loan estimate to the consumer.

If the consumer is not ready to provide the bank with their personal information, the bank can prepare an alternative document typically called a Fees Worksheet. The information below is specifically regarding the Loan Estimate but can still be used to help understand a Fees Worksheet or any other estimates prepared by the lender. Be aware, a Loan Estimate is a formal legally binding document whereas the Fees Worksheet is not.

Locked Rate VS Unlocked Rate

Before we get into the loan estimate, its important to understand the difference between a locked and unlocked interest rate. If a consumer would like to proceed with a lender, they will need to decide if they want to lock-in the interest rate. If a rate is not locked, the consumer is at the mercy of the market. Meaning, if they don’t lock and rates improve, they will get the benefit of the lower rate or vice versa. It’s important to have this conversation with the loan officer/bank before proceeding with any loan offer. Also, when a rate gets locked, there are lender related fees that should also be locked along with the rate. For example, if a consumer locks the rate with zero points/origination, the bank cannot later add points to the loan unless an extenuating circumstance happens that causes a major change in the loan itself. Assuming there are no changes to the loan, it is illegal for the bank to add certain fees such as points or processing fees after the locked loan estimate has been disclosed. We provide some more details below.

What is a Loan Estimate

The Loan Estimate is a preliminary estimate on all fees and loan terms such as the interest rate, term, loan amount, fixed/adjustable rate, etc. This document is standard across the country so Colorado residents will be looking at the same document as others who live in other States. A Loan Estimate can be disclosed before an interest rate is locked or after. If the Loan Estimate reflects a locked rate, the lender is obligated to honor that interest rate and certain fees unless an extenuating circumstance arise such as switching to a completely different loan program, changing the loan term(30 year to 15 year), change in property value or other unexpected factors that arise during the loan process. At the time of the lock, the loan officer/bank should be able to explain to the consumer if there is any potential for the interest rate or fees to change in the future.

How To Read a Loan Estimate

The LE is a very thorough 3-page document but only a few parts are important when shopping for the best mortgage offer. This does not mean that other closing costs are not important. There are 3rd party costs that lenders do not control so we want to focus specifically on the costs that a lender does control. When comparing mortgage offers, you will want to review 3 items that we will cover below. Make sure that you are comparing the same loan program with each lender. For example, if you are comparing an FHA loan to a conventional loan, the loan estimates will be drastically different. Print out a full Loan Estimate here.

Page 1/Item #1 of the LE – Interest Rate

On page 1 you will find the summary of your loan. This will give you the loan interest rate, the length of the loan, the type of loan(fixed or adjustable), and whether the loan has a balloon or prepayment penalty. Review page 1 to make sure the interest rate, and monthly payment are as you have requested. This estimate will also include property taxes, homeowners insurance and other 3rd party obligations like HOA(Homeowners Association). You will also want to clarify if your loan has mortgage insurance. Mortgage insurance is a monthly fee that is added to your monthly payment and affects your APR(annual percentage rate) so make sure you know how much your mortgage insurance is and if and when it can be removed.

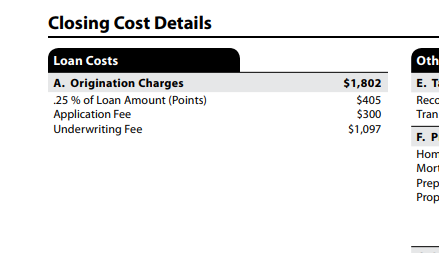

Page 2/Item #2 | Box A(Origination Charges) of the Loan Estimate

Now that you’ve compared the interest rate, we can move on to the closing costs on page 2. The screenshot below is where you will be comparing the lender fees(Loan Costs). All lender related fees go into Box A. Origination charges. You will see the breakdown below such as an underwriting fee, processing fee, etc. It doesn’t really matter what the combination of fees is because as the borrower, you will be paying for all of them. You want to just look at the total of all of the origination charges in bold. All other fees on the loan estimate are 3rd party costs and/or related to escrow(taxes/insurance). Box B does have some fees that the lender charges but that is usually for 3rd party vendors such as credit reports and appraisals. Lenders do not receive any compensation on fees listed in Box B.

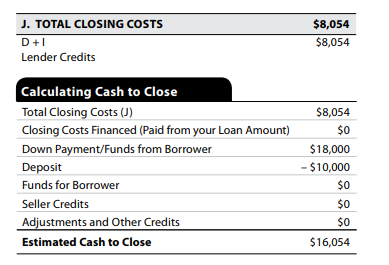

Page 2/Item #3 – Lender credit – VERY IMPORTANT

What is a lender credit? This is a rebate or credit that the lender gives you to help pay for the closing costs. So for example, if your closing costs are $5,000 and the lender credit is $4,000, than your actual closing costs are only $1,000. The lender credit will reflect under Box J.

What is a lender credit? This is a rebate or credit that the lender gives you to help pay for the closing costs. So for example, if your closing costs are $5,000 and the lender credit is $4,000, than your actual closing costs are only $1,000. The lender credit will reflect under Box J.

Why is the lender credit important? The credit may offset any lender fees that the lender is charging in Box A. So even though Box A may look like the lender is charging a bunch of fees, if the lender credit covers those fees than you will not have to pay them. For example, a lender is charging $$4,250 in origination charges with zero lender credit vs a lender charging $6,200 in origination charges with a $5,700 lender credit. Who is offering less closing costs? Its the 2nd lender since the lender credit will cover $5,700 of the $6,200 origination fee leaving only $500 vs the first lender who is charging $4,250 origination with zero lender credit. So the 2nd lender will have $3,750 cheaper closing costs.

The Short Version

When comparing mortgage offers, you need to request a “Loan Estimate” from the lender. If lender cannot provide a Loan Estimate, ask for a Fees Worksheet or itemized estimate of the closing costs. You are comparing only 3 things:

- The interest rate on page 1. For the most part self-explanatory. This is the rate the lender is charging. Make sure you are comparing the same loan program and term. So don’t compare a 15-year term with one lender and a 30-year term with another.

- BOX A. Origination Costs(loan costs) on page 2. These are the lender fees the lender is charging including but not limited to Points, Application fees, Underwriting, Processing, and Administration fees.

- Box J(lender credits) on the bottom right of page 2. So Box J will show the closing costs minus any lender credits which will give you the final/total closing costs. The lender credit will offset loan costs in Box A. Origination Charges and/or 3rd party costs such as escrows, title insurance, etc.

All other figures on the Loan Estimate will essentially be the same with every lender including escrows(Boxes E-H), title charges, and other 3rd party fees(Box B-C). Don’t get overwhelmed when comparing Loan estimates. Focus on the 3 items above!

Is It Just About Rates and Fees?

Although shopping for the lowest interest rates and fees is crucial when you’re trying to find the right lender, other factors may also be important. Lenders will have different loan programs and guidelines that may impact the client’s decision. In some cases, the client’s financial situation may limit them to work with only a certain lender(s). Location may also play a role when considering which lender to work with. We hope this information has been beneficial to you and look forward to answering any questions you may have!