FREDERICK | COLORADO USDA MORTGAGE PROGRAM

WHAT IS A USDA LOAN?

USDA residential loans are zero-down mortgages for low to moderate-income households either refinancing a current USDA loan or purchasing a home within the allowed rural locations in Colorado. USDA mortgages are zero down 100% loans. There are two types of residential USDA loans – the 502 GUARANTEED and 502 DIRECT.

The 502 Direct program is intended for low-income households and offers incredible incentives. The income limits are very strict although with rising home prices, limits have become more lenient and may be a great option for some borrowers. Borrowers interested in the 502 Direct program must apply directly with USDA. Banks do not originate 502 Direct loans. More details are below.

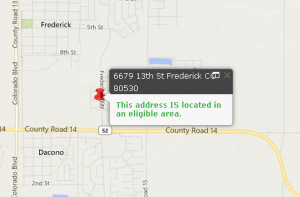

The majority of homebuyers will most likely be looking at the 502 Guaranteed program which offers more lenient income limits and a much easier loan process. Great news! The City of Frederick and surrounding areas are eligible for USDA financing! We have included the most important guidelines and benefits of USDA below.

USDA 502 GUARANTEED PROGRAM INFO (MODERATE INCOME)

$118,150 Maximum Yearly Income for 1-4 Person Household(Updated 2023)

$155,950 Maximum Yearly Income for 5+ Person Household(Updated 2023)

- 100% Financing | Zero down.

- 30-year fixed loan.

- Competitive interest rates.

- Requires a 620+ credit score.

- Discounted monthly mortgage insurance compared to FHA and conventional loans.

- Must occupy the property as a primary residence.

- Strict debt-to-income ratio requirements.

- Minimum Loan Amount $50,000 / No maximum Loan Amount.

HOW TO APPLY FOR THE USDA GUARANTEED PROGRAM

Contact us so we discuss your situation and see which program will be the best fit. We also encourage you to visit the USDA portal which offers a self-assessment tool that may help guide you in the right direction. If you believe you are on the cusp of qualifying, our USDA Guaranteed income page offers some additional details on possible deductions that may help with qualifying.

- MORE DETAILS REGARDING GUARANTEED INCOME LIMITS

- USDA GUARANTEED INCOME ELIGIBILITY SELF-ASSESSMENT TOOL

- GENERAL PROPERTY ELIGIBILITY

USDA 502 DIRECT PROGRAM HIGHLIGHTS (LOW INCOME)

$69,600 Maximum Yearly Income for 1-4 Person Household(Updated 2023)

$91,850 Maximum Yearly Income for 5+ Person Household(Updated 2023)

- Strict income limits. Intended for low and very-low income households.

- 100% Loan | Zero down.

- 33-year fixed loan up to 38 years for very low-income household.

- Subsidized mortgage. The monthly payment/interest rate is adjusted based on income.

- Current interest rate is 4.75% as of December 2023.

- Typically requires 640+ credit score.

- No mortgage insurance + Limited/zero closing costs.

- Must apply directly through USDA. Lenders DO NOT OFFER USDA Direct loans.

- Must occupy the property as a primary residence.

HOW TO APPLY FOR THE USDA DIRECT PROGRAM

To apply for the USDA Direct program, there are 3 options available:

Option 1. Contact a USDA intermediary so they can guide you through the process. Intermediaries are typically local nonprofit government agencies and approved government housing authorities. List of qualified USDA Direct government agencies.

Option 2. Apply online through the USDA portal. Create account and register.

Option 3. Schedule an appointment with a local USDA office.

Before you attempt to apply for the USDA direct program, we encourage you to speak with us first so we can evaluate your situation to see which program you will be eligible for. The process to apply for USDA Direct is completely different than the traditional loan process of applying with a lender. We can analyze your income to see if applying for the USDA direct loan will be worth your time and effort.

- USDA DIRECT GENERAL DETAILS

- USDA DIRECT INCOME ELIGIBILITY SELF-ASSESSMENT TOOL

- USDA DIRECT APPLICATION PACKAGE & REQUIRED DOCUMENTS

- LIST OF LOCAL USDA OFFICES IN COLORADO

- LIST OF COLORADO USDA DIRECT APPROVED INTERMEDIARIES

USDA ELIGIBLE PROPERTIES

- Single Family Homes.

- New construction (Construction must be completed or in process)

- Duplex.

- Log Homes w/functioning utilities.

- HUD, VA, Fannie Mae, Freddie Mac approved condos.

- Townhomes.

- Storage buildings/workshops are acceptable.

- No maximum acreage limit. Property must be typical for the area AND the value of the land should not exceed 30 percent of the property value.

- No income producing properties. Home based businesses are okay.

- Farms not allowed but farm animals are okay as long as not for income producing purpose.

- The guaranteed USDA program is not intended to purchase land only.

- Manufactured homes are not eligible unless the property is currently financed by USDA.

WHAT WE DO FOR OUR BORROWERS

- Excellent customer service. As a local lender, we take pride in the service we provide to our clients.

- Extremely competitive mortgage rates and low closing costs.

- Ability to cover closing costs. Why is this important? Even though USDA is 100% financing, closing costs cannot be added to the loan. In some cases the seller may cover closing costs but in a situation where this is not an option, we have the ability to provide the buyer a credit to help pay for some or all closing costs. This is done by giving the buyer a lender credit in return for a slightly higher interest rate.

USDA | FHA | CONVENTIONAL (Which is Better)

- FHA requires 3.5% down payment / Conventional requires 3/5% down. USDA does not require a down payment.

- FHA interest rates will typically be lower than USDA Guaranteed & conventional loans but USDA has lower monthly and upfront mortgage insurance. USDA Direct will have lower rates, less fees, & no mortgage insurance.

- USDA loans do not have maximum loan amounts. FHA and conventional loans have restrictions based on County limits.

- FHA and conventional loans have no restrictions on location but USDA is limited to eligible rural areas only.

- USDA loans have strict underwriting rules compared to FHA and conventional loans, specifically debt to income ratio requirements.

- USDA mortgages have household income restrictions. FHA and conventional loans do not have income limits.

- Conventional loans might offer better terms if buyer/homeowner has a high credit score and large down payment.

- USDA and FHA have strict appraisal requirements compared to conventional loans.

THE LOAN PROCESS

- Borrower must complete a loan application. This can be done online through a secured portal or over the phone.

- We will run the loan application through an automated underwriting system called GUS. The application will either be automatically approved or the loan will need to be manually reviewed by an underwriter.

- If the application is not approval through GUS, we will submit the loan to underwriting to review the applicant’s income and credit. This process typically takes a few days.

- Once the pre-approval is complete, we will issue a pre-approval letter so the applicant can begin house hunting.

If you’re looking to buy a home in Frederick, the USDA guarantee program may be a great option if you have good credit and your income is under the Weld County household income limits. Contact us if you have any further questions or concerns.