FORT MORGAN | COLORADO USDA LOANS

WHAT IS THE USDA GUARANTEED MORTGAGE

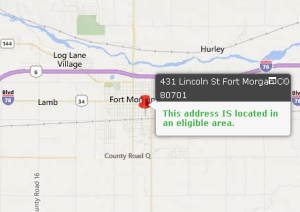

A USDA loan is a zero down residential mortgage program intended for rural areas in the United States. The purpose of the program is to encourage home ownership in rural areas with lower populations. The entire City of Fort Morgan is eligible for USDA financing! Please contact us with any questions or concerns.

BENEFITS OF USDA

- 100% Zero down home loans. Can be combined with local assistance programs.

- Very competitive interest rates.

- Low monthly & upfront mortgage insurance.

- Purchase and Refinance. Can be used to purchase a new home or refinance existing home.

- Fixed secured loans – 30 Year fixed only.

- Not Required to be First-Time Homebuyer | Applicant may own ONE additional property but must occupy USDA financed property as their primary residence.

- Seller concessions allowed up to 6% of the purchase price. Can be used to cover closing costs and/or upfront mortgage insurance.

HOW TO QUALIFY FOR THE USDA GUARANTEED LOAN | ELIGIBILITY

HOW TO QUALIFY FOR THE USDA GUARANTEED LOAN | ELIGIBILITY

- Income limits are based on County. Fort Morgan is located in Morgan County so household income needs to stay under the limits below:

- $118,150 Maximum Yearly Income for 1-4 person household (Updated 2023)

- $155,950 Maximum Yearly Income for 5+ person household (Updated 2023)

- Credit Score must be 620+. No exceptions to this rule. We use the middle credit score of all borrowers applying for the mortgage.

- Must occupy the home as a primary residence. Cannot be used to purchase investment property.

- Minimum Loan Amount $50,000 / No maximum Loan Amount & No purchase price restrictions.

- Property must be located in an eligible rural area.

THE LOAN PROCESS

- Borrower must complete a loan application. This can be done online through a secured loan application or over the phone.

- We will run the loan application through an automated underwriting system called GUS. The application will either be automatically approved or the loan will need to be manually reviewed by an underwriter.

- If the application is not approval through GUS, we will submit the loan to underwriting to review the applicant’s income and credit. This process typically takes a few days.

- Once the pre-approval is complete, we will issue a pre-approval letter so the applicant can begin house hunting.

USDA ELIGIBLE PROPERTIES

- Single Family Homes.

- New construction (Construction must be completed or in process)

- Duplex.

- Log Homes w/functioning utilities.

- HUD, VA, Fannie Mae, Freddie Mac approved condos.

- Townhomes.

- HUD approved Manufactured homes / Must be on a permanent foundation.

- Storage buildings/workshops are acceptable.

- No maximum acreage limit. Property must be typical for the area AND the value of the land should not exceed 30 percent of the property value.

- No income producing properties. Home based businesses are okay.

- Farms not allowed but farm animals are okay as long as not for income producing purpose.

- The guaranteed USDA program is not intended to purchase land only.

- Manufactured homes are not eligible unless the property is currently financed by USDA.

WHY CHOOSE US AS YOUR USDA LENDER?

- Excellent customer service. As a local lender, we take pride in the service we provide to our clients.

- Extremely competitive mortgage rates and low closing costs.

- Ability to cover closing costs. Why is this important? Even though USDA is 100% financing, closing costs cannot be added to the loan. In some cases the seller may cover closing costs but in a situation where this is not an option, we have the ability to provide the buyer a credit to help pay for some or all closing costs. This is done by giving the buyer a lender credit in return for a slightly higher interest rate.

OTHER ELIGIBILITY LINKS & INFO

Use the links below to see if you’re eligible for a USDA loan. You can also contact us and we can assist you with your questions and guide you through the process.

USDA Income Eligibility Calculator

Colorado USDA Website

USDA Income Limits

USDA vs FHA vs CONVENTIONAL (Which Loan Is Better)

- FHA requires 3.5% down payment / Conventional requires 3/5% down. USDA does not require a down payment.

- FHA interest rates will typically be slightly lower than USDA and conventional loans but USDA has lower monthly and upfront mortgage insurance.

- USDA loans do not have maximum loan amounts. FHA and conventional loans have restrictions based on County limits.

- FHA and conventional loans have no restrictions on location but USDA is limited to eligible rural areas only.

- USDA loans have strict underwriting rules compared to FHA and conventional loans, specifically debt to income ratio requirements.

- USDA mortgages have household income restrictions. FHA and conventional loans do not have income limits.

- Conventional loans might offer better terms if buyer/homeowner has a high credit score and large down payment.

- USDA and FHA have strict appraisal requirements compared to conventional loans.

If you’re looking to purchase a home or refinance an existing USDA loan in Fort Morgan, USDA may be a great option assuming your credit score is above 620. Contact us if you have other questions or would like to get preapproved.